Abstract

There is no cash flow attached to COMP at this stage. However, there may be a proposal in future that allows COMP holders to capture value from platform’s usage . Currently, COMP value is derived purely from governance rights embedded into the token. When there is a value capture proposal in place COMP can be valued using DCF or multiple of TLV (Total Value Locked) along with governance premium. We do not think that valuing COMP as money is prudent in early days.

Introduction

The market for native and non-native crypto-assets has come a long way in just a decade and the ecosystem of traders, investors, and speculators has developed at a breakneck pace. However, the ecosystem is not as sophisticated as legacy financial markets, which offer a wide range of products that allow participants to trade time value of assets. Platforms that allow users to borrow assets against collateral have come in vogue after the successful launch of the Compound (COMP) token. This does not mean that there were no lending/borrowing platforms; the so-far viral success of COMP lies in its token economics. In this article, we discuss the Compound protocol, various aspects of COMP token, and how we can value it.

How the Compound protocol works

Unlike other crypto lending/borrowing platforms where users on each side are matched to borrow and lend, the Compound protocol pools and combines the liquidity of each token and then lends it to borrowers. For instance, when users deposit their USD coin (USDC), it becomes a fungible resource within Compound to make pooling and accounting easier. These are known as cTokens, so USDC becomes cUSDC and all cUSDCs are pooled. While lending, cUSDC is converted to USDC. Every asset has a collateral factor which decides the percentage of the amount a user can lend. The collateral factor for USDC at the time of writing was 75%. Borrow rate is adjusted dynamically based on the supply and demand of the particular asset. A small portion of borrow interest, known as reserve, is set aside by the protocol as insurance, and the remainder is split among asset suppliers on a pro-rata basis.

Supply APY=Borrow APY × Utilisation × (1-reserve factor)

APY = Annual Percentage Yield Reserve factor decides what percentage of the borrow APY goes to reserves which can be thought of as insurance against unexpected liquidations.

However, this mechanism was not the sole driver of the stupendous growth of the value locked in the Compound protocol. The centrepiece of the Compound attraction was the distribution of its governance token, COMP. Compound launched COMP and started distributing it on June 15, 2020. COMP is an ERC-20 token with governance rights embedded in it. Every day, around 2,880 COMP tokens are distributed based on the total value of borrowings of an asset on a given day and they are split equally between suppliers and borrowers. For example, on July 16, the total value borrowed using Compound was about USD 1.02 billion with DAI contributing about USD 810 million of the total borrowed value. Therefore, the daily COMP being distributed to DAI lenders and borrowers is about 2,287 [2880*0.81/1.02 = 2287]. So, 1143.5 COMP are distributed among DAI suppliers and 1143.5 among DAI borrowers. As users are rewarded for providing liquidity to the system, a distribution such as the above is termed as liquidity mining.

As COMP is a governance token, we must understand the crux of the Compound’s governance. It works in the following manner:

- Any address with over 100,000 COMP tokens delegated1 to it may propose governance actions. Governance proposals are executable code.

- Once the proposal is created, the community (COMP holders) may vote within three days.

- If a majority and at least 400,000 votes are cast for the proposal, they are queued in a time lock and then implemented after two days

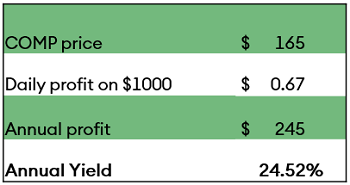

Soon after COMP token distribution commenced, it started trading on Uniswap followed by Coinbase2. Compound started trading on Uniswap for about USD 60 and, after the Coinbase listing, it briefly traded for about USD 427 before gradually falling to around USD 160. As COMP has been trading for just over a month, we think that it is still undergoing price discovery. The high price of COMP tokens allows users to lend and borrow through platform almost without any risk. We demonstrate this through the following example.

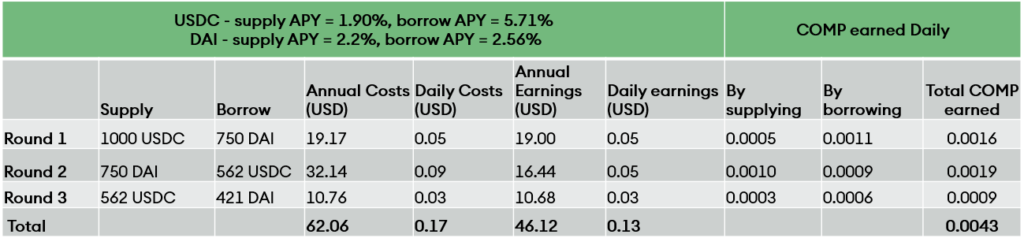

Consider that a user supplies 1,000 USDC to Compound and USDC has a collateral factor of 75%. Therefore, the user is allowed to borrow any other asset worth 750 USDC. The user then borrows 750 DAI. In the next round, the user can supply 750 DAI and borrow assets worth 75% of 750 DAI and so on.

The following table shows results of the three rounds where the user supplies and borrows assets.

Table 1 – Illustration earnings by supplying and borrowing assets using the Compound protocol

At current prices, the annual yield translates to around 25%.

Table 2 – Illustration of annual yield on Compound

A user can always switch between different assets to maximise their gains3 where additional rounds are also possible. As long as the COMP price remains high, profits with little risk are possible. Users need to be active to maximise yields as they are dynamic and the opportunities may often be short-lived.

The ability to re-supply assets creates leverage in the system and, thus, more risk. For example, there are just over 200 million DAI in existence; however, DAI supplied via compound is about 942 million, that is, Compound has 3.8X the number of existing DAI.

Why valuing COMP right now is futile

Before diving into how COMP is valued, we need to answer a few questions. Is the COMP token required? Why should COMP have any value at all?

Theoretically, the platform can function without an embedded token; the team aims to decentralise governance and COMP represents a vote in that process. Votes could be dynamically distributed based on the value locked in the protocol, and delegation could work in the same manner. For example, if each vote is worth USD 1, a user who supplies USD 1,000 worth to the protocol can delegate 1,000 votes to another user without an ERC20 token; but, it would still have to be accounted for, and it makes accounting easier if there is a separate token. Moreover, the team was funded by venture capitalists (VCs) for building the protocol. Therefore, how do the VCs and the team aiming to build a decentralised money market protocol benefit from it? In this context, the team and their VCs building a public good get funded through a token. Thus, the token becomes vital.

Unlike for MakerDao, there is no value capture mechanism on Compound at present4, meaning that there is no spread between borrowers and suppliers which goes to the protocol. Only a reserve factor exists for every asset, which can just be thought of as rainy-day insurance. Therefore, in traditional terms, there are no expected cash flows attached to COMP tokens. Does this mean that COMP should have zero value? In our view that would be premature to declare it worthless on these grounds; there could be two reasons for ascribing a non-zero value to COMP.

First, although there exists no value capture mechanism now, there could be one in the future. Token holders can propose a change to charge a small fee to users which gets distributed among COMP holders. Alternatively, users may propose other means of capturing value. At the moment, early-stage start-ups can be thought of as analogous to Compound’s no-spread model. Start-ups funded by seed investors are often encouraged to capture customers without requiring significant customer spending during the early days. In other words, costs are borne by investors during the early stages on the premise of acquiring expected returns later. Similarly, early investors of Compound are funding the growth of the platform now.

Second, there are discussions on treating COMP as money. Like bitcoin, COMP tokens can also be thought of as money. Money is a belief system; it is a social contract. Just as there are investors who believe that bitcoin has value, there are those who believe that COMP has value as well. However, we believe that COMP is a far lesser form of money than bitcoin because of several reasons, as elaborated below:

- COMP is not a native token as the platform is built on Ethereum; Ether secures it. Therefore, platform security is dependent on Ether and not on COMP, which exists to fund the team building a public good.

- COMP derives its value, if at all, from the governance; and the governance is only strong when COMP (or the votes) is well distributed. Currently, it is far from well distributed. The first account on the leaderboard has more than 345,000 votes while the 100th account has just 4 votes.

- Bitcoin miners need to sell BTC to cover their operational expenses. In a way, the distribution of BTC is a forced by-product of incentivising network security. The same cannot be said about liquidity miners who earn COMP tokens by supplying liquidity to the protocol. A wider distribution of COMP is necessary for successful governance; the current method of distribution does not ensure COMP’s wide distribution.

- Bitcoin has gained trust over the years. The network effects of bitcoin are far higher than any other cryptocurrency that claims or aims to be money.

Therefore, the journey for COMP being regarded as money is long and fraught with obstacles. And COMP as money is not the best of arguments to justify its current price.

Should every COMP have equal value?

COMP derives value from governance. An account that holds 10,000 COMP is virtually worthless against an account that has 340,000 COMP. In practice, users will pay incrementally more to acquire COMP in case of a tie. In that case, each token should not have the same value. COMP in larger accounts should get a premium.

Possible ways of valuing COMP

The first way to value COMP is to discount expected cash flows, just as few have done in the case of Maker (MKR). However, the valuation exercise cannot be performed now as there are no such proposals and making any assumptions may be rendered useless. Nevertheless, we think that it is not too far-fetched to assume that at some point there will be a proposal that suggests a certain value capture mechanism for COMP holders.

The second way could be based on multiples of total loans issued, as done for traditional businesses. The catch here is that traditional businesses are given multiples with an assumption that their loan book will generate non-zero revenue. Without any value capture mechanism, assigning a multiple to total loans generated by the Compound protocol may not be prudent.

Thirdly, it can be valued as money but we do not think that as this stage it is a prudent argument.

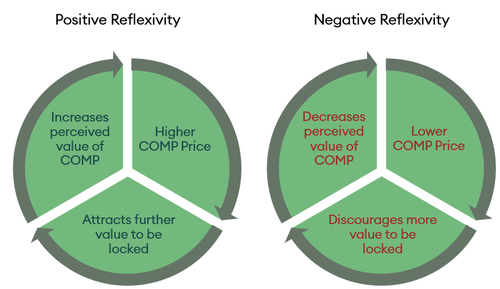

How reflexivity affects COMP price

In 1987, legendary investor George Soros published The Alchemy of Finance wherein he mentioned the theory of reflexivity. It states that investors’ views are imperfect, and they are shaped by what they believe. For example, if investors think that markets are efficient then their belief influences the way they invest and this, in turn, changes the nature of the market.

What does COMP have to do with reflexivity? Value locked in Compound is linked to COMP price as COMP price allows users to earn risk-free profits. The more value people think COMP has, the more will be value locked to earn more COMP, further increasing the value. When an alternative to COMP arises such as Yearn Finance5, value locked in Compound seeks a new shelter to earn more profits, thus, lowering the perceived value of COMP. It then acts as a headwind for COMP.

COMP Reflexivity

Conclusion

There is reflexivity associated with COMP. Competition could reduce the allure of the Compound protocol. Permissionless and open-source nature of DeFi allows the code to be forked. When there’s a platform with rewards more attractive than those of Compound, capital will flee to that platform.

We think that COMP has non-zero valuation because there will be a value capture proposal in future. Once the path to value capture is known we can make assumptions and value COMP.

1Users can delegate their votes to addresses they do not control. ↵

2Coinbase is also one of the VC investors in Compound Labs Inc. ↵

3Given the constraints such as supply and borrow APY, and collateral users may choose to optimise for the best pair. Readers should bear in mind that the current gas fees on Ethereum are very high. As a result switching costs may be prohibitive and may render the exercise counterproductive. ↵

4In simple terms, MakerDao is like a decentralised central bank. Users borrow DAI against collateral. And the platform charges users a fee to perform operations that keep DAI at USD 1. This fee is used to burn MKR tokens as a mechanism to distribute value to MKR holders ↵

5Yearn Finance has already started attracting value from Compound ↵