Executive Summary

- We continue to navigate the crypto market cautiously, with a preference for low beta coins such as bitcoin and ether

- As prices have declined massively in May in the wake of the Terra debacle, dragging sentiment further down to an extreme level and improving valuation, we have reduced our cash position

- Our macroeconomic scenario remains cloudy. While inflation has peaked, it remains a concern. Supply chain bottlenecks and loss of purchasing power combined with higher interest should weigh the growth forecast. The critical question is whether central banks will continue fighting against inflation as announced or accommodate for lower growth

- Solana has experienced repeated issues in the last month, and its future is uncertain

- The entire DeFi ecosystem has been hit significantly due to Terra’s fall as the total value locked (TVL) across blockchains and protocols has been cut in half from approx. USD 200 billion to approx. USD 100 billion

- The NFT ecosystem contributes to most of the activity on the Ethereum network. It peaked at all-time high levels in the beginning of this year but has been declining since last month, given the overall negative market sentiment

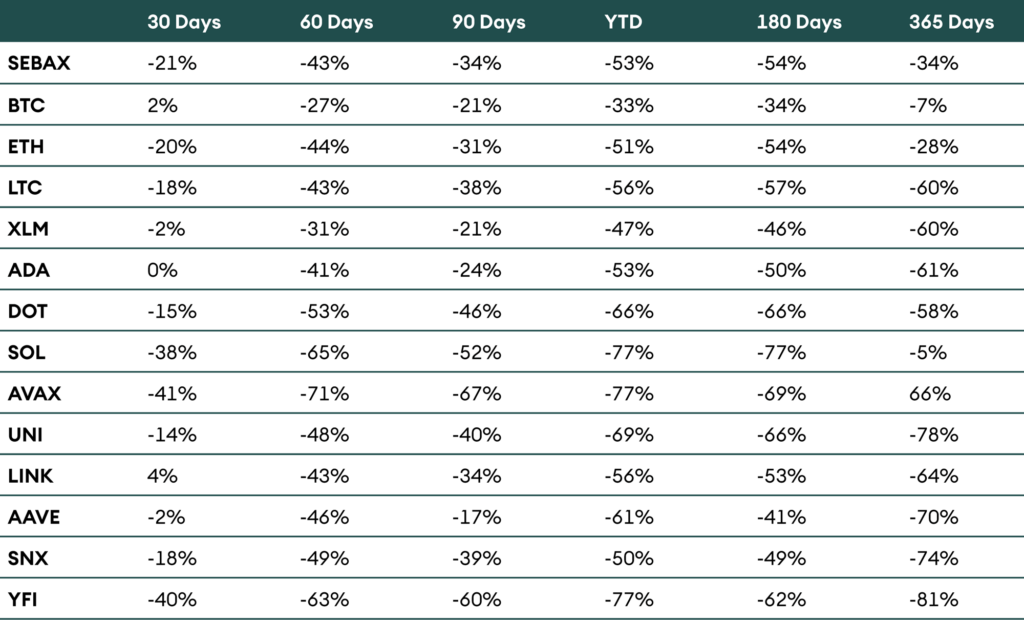

Table 1: Performance of AMINAX® and AMINA coin universe assets as of 7 June 2022

Outlook

The Terra Luna debacle dominated the crypto news flow last month as it triggered one of the biggest crypto market crashes on record. The Terra Luna (LUNA) blockchain and its algorithmic stablecoin TerraUSD (UST) proved unstable. The combined market capitalization of these two assets was close to USD 50 billion days before the crash. It is worth close to nothing today.

In the wake of this debacle, the overall crypto market capitalization dropped by more than USD 500 billion to USD 1.2 trillion. In the second half of the month, prices have somehow stabilized.

The AMINAX® Index, a selection of blue-chip cryptocurrencies, fell by 21% in the last 30 days. Notice that the AMINAX® Index did not contain LUNA. The leading digital asset, Bitcoin (BTC), is up by 2% for the month, and the second-largest protocol or the leading smart contract platform, Ethereum (ETH), is down by 20% in the same period. Traditional markets were also highly volatile last month, but the order of magnitude is considerably smaller: S&P 500 is up by 4.2%, and NASDAQ is up by 4.7%.

Our last month’s Digital InvestorDigital Investorlink1 title was “Cautiously navigating crypto” because of the weak economic scenario dominated by high inflation, aggressive Fed, and slowing growth, a scenario we thought detrimental for growth assets. As the correlation between cryptocurrencies and the NASDAQ is high, we decided to invest cautiously in crypto. Consequently, we favoured bitcoin and ether over all other digital assets, be it alternative platform blockchains or Decentralised Finance (DeFi) tokens, and held cash.

While inflation remains a concern as we advance, the market implications have changed. Late last year and early this year, rising inflation was synonymous with change in monetary policy; inflation today is closely associated with purchasing power reduction and bottlenecks, in other words, with growth concerns. As the narrative changes, the Fed and other central banks may deliver less monetary tightening than expected.

As far as cryptocurrencies are concerned, the macro landscape is likely to weigh on sentiment. More specifically, sentiment in cryptocurrencies is negative as fear dominates. Ongoing issues with Solana, an innovative platform aiming to offer fast (scalable) and cheap transactions, plagued sentiment further. Solana has recorded repeated downtime in the last month due to multiple issues.

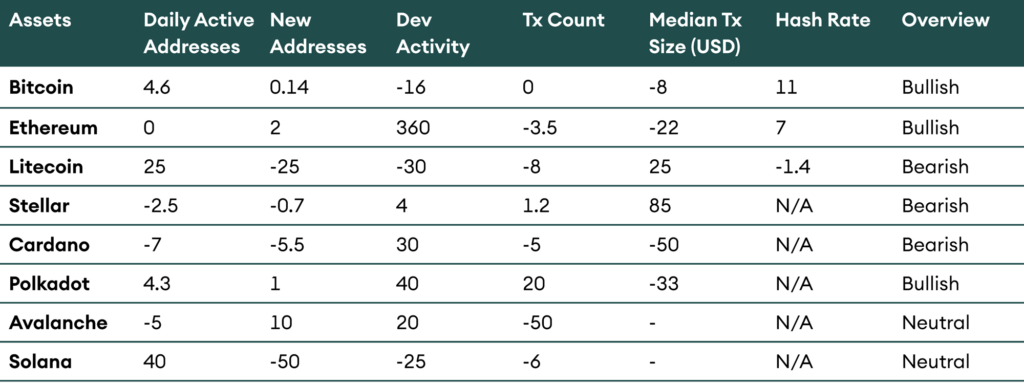

We continue to navigate crypto cautiously and prefer established coins such as bitcoin and ether over all other currencies. First, they are low beta digital assets, and second on-chain activity statistics remain solid, as shown in table 2. Notice that Polkadot on-chain statistics are also supportive. Remember that our tactical asset allocation is not only based on on-chain statistics.

More generally, the price performance of cryptocurrencies since the beginning of the year has been disappointing. The “best” coin, bitcoin, lost more than a third of its value in the year’s first five months. Overall, prices are depressed today, and valuation has improved sharply as a result. We have tactically reduced our cash allocation due to attractive valuation and depressed sentiment.

Table 2: On-Chain Activity Overview – 30-day percentage change for all parameters (as of 26 May 2022)

Bitcoin

Bitcoin price fell significantly last month, dragging the overall market down with it, but has since recovered and recorded an overall gain of 2% in the previous 30 days. But the same cannot be said about the performance of other digital assets, as most of them are still at negative returns in that same period. It reflects the maturity of this asset as compared to some of its competitors.

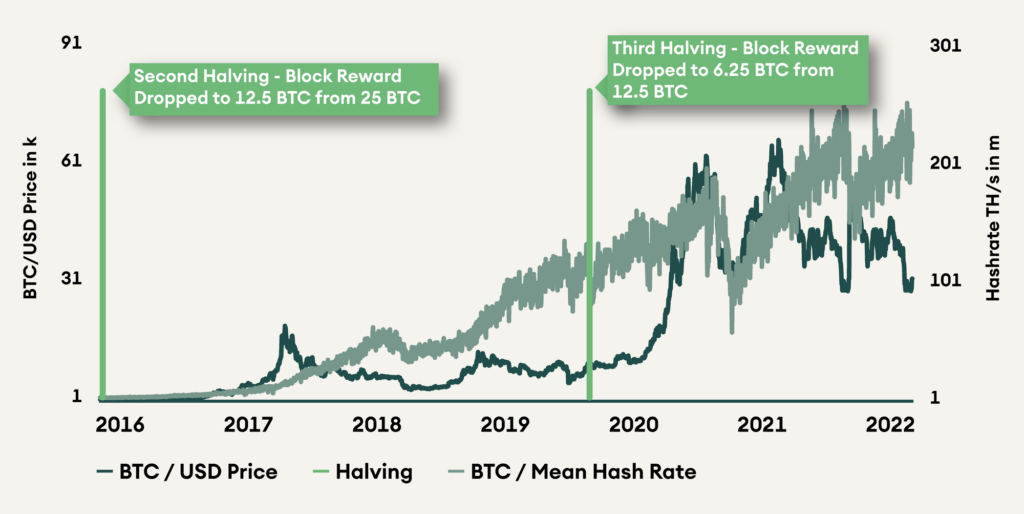

The perception of bitcoin being a store of value and an inflation hedge is challenged as the price has declined at the same time as inflation has accelerated. It, however, didn’t prevent bitcoin from showing increasing adoption. Figure 1 suggests continuous support, as the hashrate, an indicator of mining activity, has continued to grow despite the price decline.

Figure 1: Bitcoin Price & Hashrate with Halving (Data as of 31 May 2022)

Bitcoin hashrate has fully recovered after the 2021 drop caused by the Chinese mining ban, and it is now at all-time high levels. As the hashrate increases, it becomes increasingly difficult to attack and gain an advantage, enhancing the network’s security.

Evidence shows that large bitcoin holders take advantage of the price decline and accumulate. Glassnode has developed an ‘Accumulation Trend Score’ indicator to quantify this behaviour. It has been close to 1 for the past month and is the highest in the last six months.

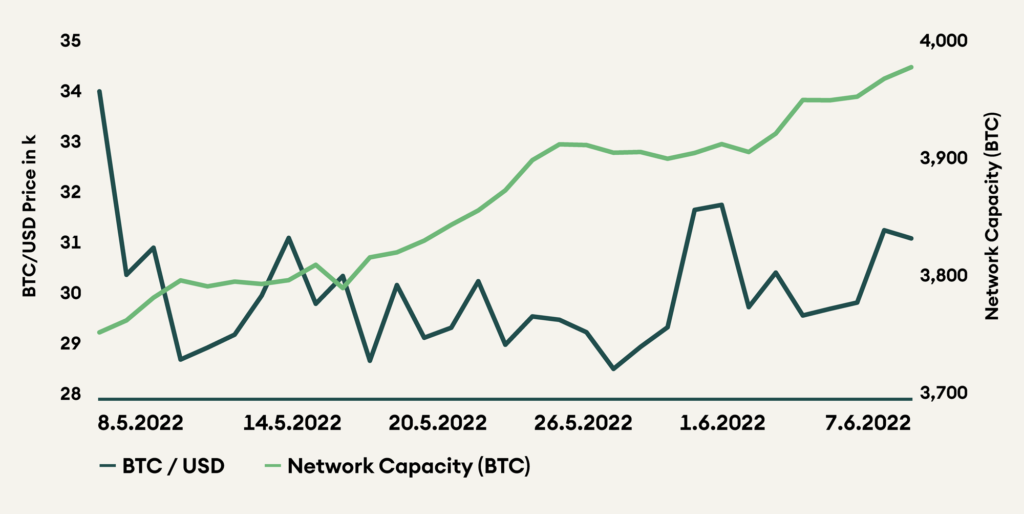

Lightning network capacity has increased further to reach 4,000 BTC (Figure 2), signalling it is used more and more as a medium of exchange for fast and cheap day-to-day transactions.

Figure 2: The Lightning Network Growth (Data as of 7 June 2022)

Paradoxically, blockspace demand has slowed for both Bitcoin and Ethereum in the past few months and stands at multi-year low levels, resulting in low transaction fees. Bitcoin network transaction fees have declined significantly since mid-2020 due to network upgrades, such as SegWit and the Lightning Network. They reduce the amount of data stored in each block and process transactions by batching them together. However, the network transaction fees spike up during a time of high volatility and high demand for blockspace; it can be observed during the Luna crash.

On a different topic, El Salvador conducted a three-day conference for central bank officials. The event gathered 44 central banks from developing countries worldwide to discuss financial inclusion and educate them on Bitcoin. Notice also that 7.5% of all BTC that will ever exist is held in multiple ETFs, government treasuries, and public or private companies. Read the latest Crypto Market Monitor for more information on these topics.

Ethereum

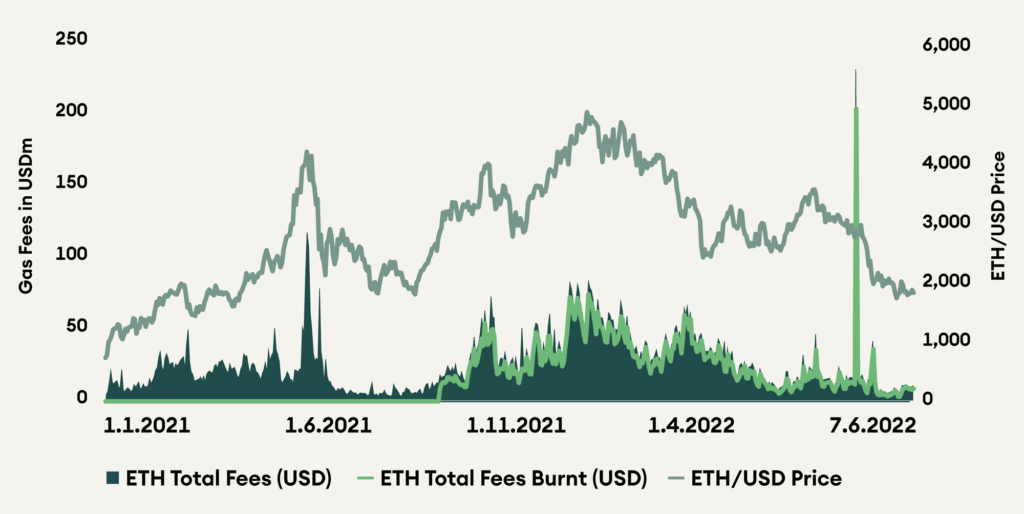

Ethereum has the most extensive decentralised application (DApp) ecosystem among all smart contract platforms. Still, the demand for blockspace on this network has also significantly decreased in the last month, resulting in low gas (transaction) fees. This affects the rate at which ETH is being burnt through transaction fees post the implementation of EIP 1559, and it is at an all-time low. As in the case of Bitcoin, there are spikes in gas fees during times of high demand. It is a common occurrence during some high-profile NFT mints. Still, gas fees on the Ethereum network have been decreasing since November 2021, the beginning of the current bear market cycle.

Figure 3: Ethereum transaction total fees with fees burnt post-implementation of EIP 1559 and USD price (Data as of 7 June 2022)

In efforts to make Ethereum more scalable and thus more widely adopted and used by people from across the world, the consensus algorithm for the network is being moved from proof of work (PoW) to proof of stake (PoS). For this purpose, a coordination network was launched in December 2020 called The Beacon Chain. It acts as the key consensus layer in the expanded network of shards and stakers. But it cannot handle accounts or smart contracts like the Ethereum mainnet today.

The Beacon Chain has approximately 12 million ETH (USD 24 billion) staked as of today, with 398k validators securing the network. The upgrade that will transition Ethereum from PoW to PoS is called The Merge, and it is expected to be implemented by August 2022. But the Beacon Chain has been launched for the testnet Ropsten, which will serve as the testing ground for the new blockchain.

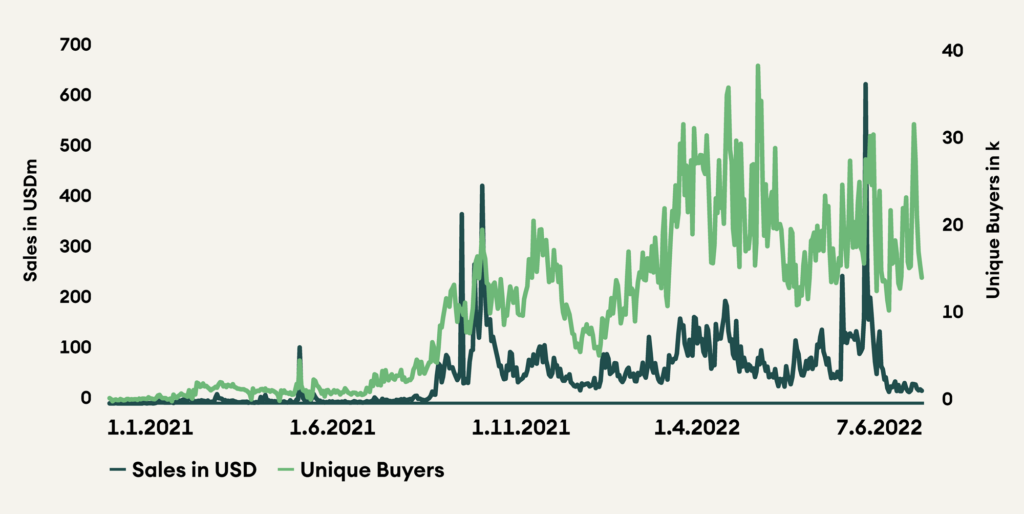

Figure 4: Daily NFT sales volume, with number of unique buyers on Ethereum (Data as of 7 June 2022)

Ethereum has the most extensive NFT ecosystem of all smart contract blockchains, followed by Solana and a few others. Most of the transactions on the Ethereum network today come from NFTs. A few months ago, DeFi activity explained most of the transactions. After the all-time high levels of sales volume and number of unique NFT buyers in the first few months of this year, we are now witnessing a decline in those numbers, given the overall negative sentiment in the market.

Alternative Blockchains

Besides the two leading networks, Bitcoin (BTC) and Ethereum (ETH), alternative blockchain prices declined even more. Litecoin price (LTC) dropped by 18% in the last 30 days, Polkadot (DOT) by 15%, Solana (SOL) by 38%, and Avalanche (AVAX) by 41%.

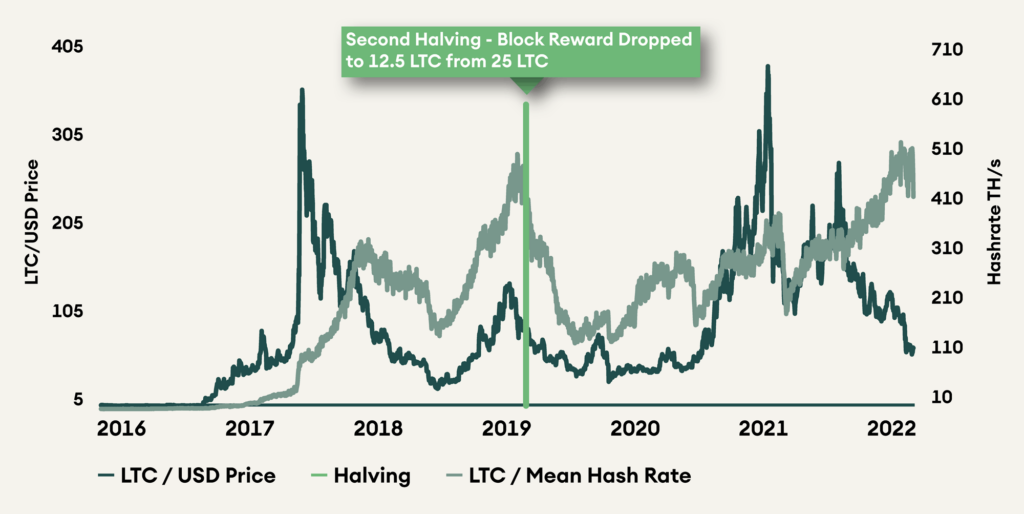

While Litecoin has existed for many years, it has failed to generate exponential returns. It touched the all-time high price in early 2021 and has trended downward since then. The same is true for the network hashrate; it peaked last month but is at the same level as of 2019 and failed to break out from that level. Interestingly, the network hashrate significantly dropped after the second halving of the miner rewards in August 2019. It is unusual as Bitcoin hashrate continued to grow even after halving events.

Figure 5: Litecoin Price & Hashrate with Halving (Data as of 31 May 2022)

The first two batches of Polkadot parachain auctions are complete, and 18 slots have been allocated. A 131 million DOT (USD 1.3 billion), 11% of the total supply, is locked in parachains and crowdloans. The third batch of auctions for slots 19-25 started on 5 June and will conclude on 23 August. Transaction count on the Polkadot network is increasing, as seen in the on-chain activity table at the beginning of this article.

Avalanche is gaining new users, but the transaction count and daily active addresses were down last months, whereas developer activity has increased. Avalanche has failed to create momentum around NFTs as Solana did. But Solana is having its own set of trouble.

The Solana blockchain saw a few network outages last month; the main reason for this is the excessive transactions generated by bots. This affects all the ecosystem participants and questions the long-term sustainability of the blockchain. The most recent downtime has been caused by a known bug that was not fixed, and the network clock is running six hours behind the world clock, leading to losses for validators. This blockchain is going through some tough testing times, and it is difficult to predict its future now. It can only sustain if the outages are stopped; otherwise, the project might shut down.

Decentralised Finance (DeFi)

The fall of Terra Luna had a dramatic impact on DeFi. The Terra algorithmic stablecoin UST played a central role in many DeFi protocols. Its fall sent shock waves across the board. Other stablecoins in the ecosystem were also affected. The most popular stablecoin Tether (USDT) unpeg for a brief period before going back to parity with the USD. The circulating supply for USDT and DAI reduced, given the less transparent reserves for Tether and volatile crypto collateral for DAI, indicating reduced trust in the system.

On the other hand, Circle (USDC) and Binance (BUSD) witnessed an increase in the circulating supply as the faith shifted towards a transparent and stable reserve of these assets. We discussed this in more detail in one of last month’s Crypto Market Monitor. Please read it here.

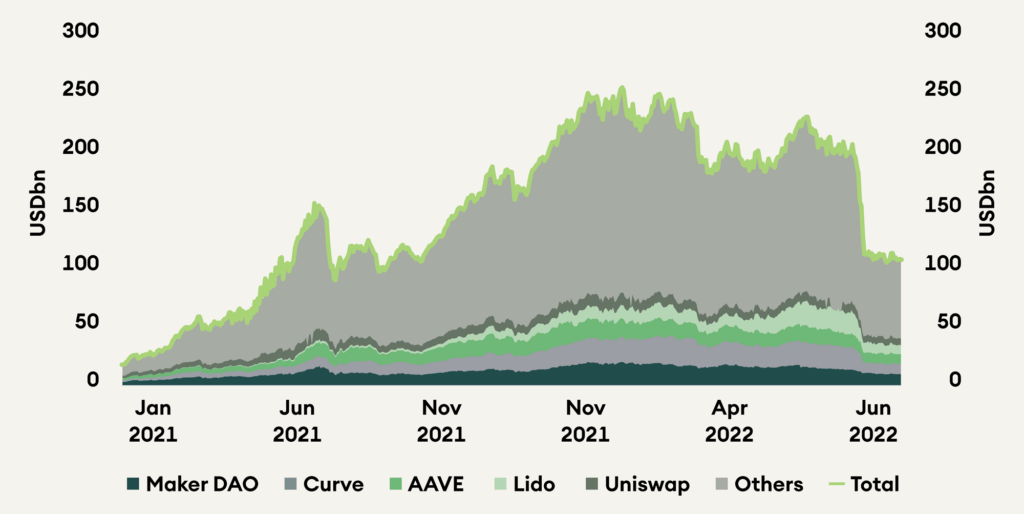

Figure 6: Total Value Locked (TVL) across chains in DeFi, with key contributors (Data as of 7 June 2022)

NFTs have already taken up the crown of most transactions on the Ethereum network from DeFi in the past few months. We have seen a decline in the new user growth for DeFi, resulting in low activity. Total value Locked (TVL) across different blockchains and their DeFi protocols stood at USD 240+ billion in November 2021. But the market declined, bringing it to USD 200 billion by 1 May 2022, and then following the Terra fall, TVL was cut in half within a month and now stands at approx. USD 110 billion.

The lack of new users and the low activity in DeFi protocols can be attributed to many reasons, such as lack of right incentives, security, and regulatory concerns, lack of proper education, and rewarding user experience. We hope to see innovation in the DeFi space that can revive the lost momentum.

Conclusion

Developments in macroeconomic conditions will continue to determine the direction of traditional and digital markets. Between inflation and the risk of recession, a stagflation scenario is developing. The overall sentiment is poor among investors. A lot depends on the Fed’s move to either hike rate as expected and choose inflation or provide some room for the market if it considers the growth slowdown. Needless to say, the risk of war breakout and supply chain bottleneck cast a further shadow on the outlook.

Besides the cloudy outlook, the fall of the Terra ecosystem and its flagship algorithmic stablecoin UST undermined investor sentiments and raised the need for regulation. Finally, the repeated issues of the Solana chain weighed further on sentiment.

We continue to navigate the market cautiously, preferring low beta cryptos such as BTC and ETH over alternative platforms and DeFi. However, as the sentiment is very negative and prices have corrected significantly, we have reduced our cash position.

Bitcoin and Ethereum on-chain activities have remained solid, suggesting they are valued attractively.